How much can I gift to my grandchildren?

The relationship between grandparents and grandchildren is often a treasured part of family life. And with the high cost of education and housing in the UK, it’s only natural that grandparents want to help their grandchildren in any way they can. In this article, we’ll look in more detail at how much money you can gift to your grandchildren, and how this compares to gifting to your children.

How much can I give my grandchildren tax-free?

From school fees and university to putting money towards a deposit, gifts of money from grandparents can make a real difference to grandchildren’s lives. And based on the current Inheritance Tax (IHT) exemptions, giving little and often could help you reduce or avoid any IHT liability.

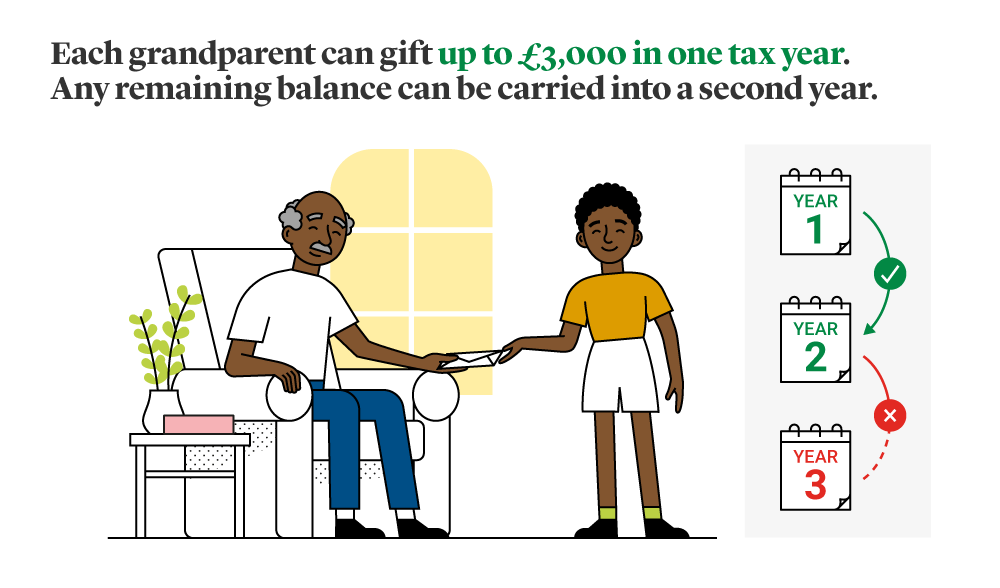

So, how much can you gift to your grandchildren tax-free? Each grandparent can gift up to £3,000 in any one tax year, exempt from IHT. If the whole £3,000 is not used in any single tax year, the balance can be carried forward to the next tax year. So if you make no cash gifts in one tax year, you can give away a total of £6,000 in the next tax year. However, any unused is lost if not utilised in the next year. In short it cannot be carried forward to year 3. This exemption applies to lifetime gifts.

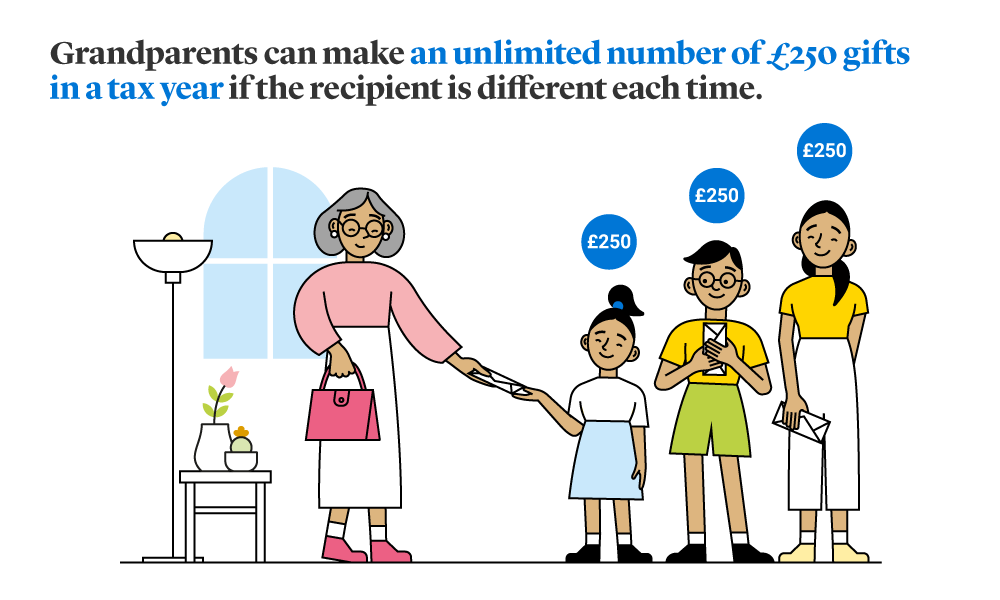

It’s also possible to make an unlimited number of small £250 gifts in each tax year so long as the recipient is a different person each time. What’s more, there are exemptions of up to £2,500 for gifts made in respect of a grandchild (or great-grandchild’s) wedding or civil partnership; this increases to £5,000 if your own child is tying the knot.

Gifting money to grandchildren

Before you decide how much to gift to your grandchildren, you’ll understandably want to know how this compares to gifting to your adult offspring.

How much can you gift tax-free to children?

As with gifting to grandchildren, you can give away up to £3,000 worth of gifts tax-free to your children in a single tax year. This is known as your annual exemption. Technically, you can gift as much money to your children or other family members as you like, but in order for your gift to be Inheritance Tax-free, you would need to live for at least seven years from the date the gift is made. This is what is known as the seven year rule for gifts – officially known as a Potentially Exempt Transfer (PET) – which we’ll cover in more detail later. Note that there may still be Capital Gains Tax due when gifting money to children.

How Inheritance Tax works with gifts

Lifetime transfers

Once your total chargeable lifetime transfers in the last seven years has exceeded the IHT threshold of £325,000, tax will become payable at the lifetime rate of 20%.

Tax is charged on the ‘transferor’, which in this case could be the grandparents, but it can also be paid by the transferee (the grandchildren). The amount of tax paid can be affected by who pays the tax.

Tax is due six months after the end of the month in which the transfer is made, or for a transfer made after 5 April and before 1 October in any year, the due date is the end of April in the next tax year.

Potentially Exempt Transfer

A Potentially Exempt Transfer (PET) enables an individual to make gifts of unlimited value which will become exempt from IHT if the individual survives for a period of seven years.

If this doesn’t happen, the PET becomes a Chargeable Consideration, and is added to the value of your estate for IHT. If the combined value is more than the IHT threshold, IHT may be due.

If the donor dies within seven years from the date of the PET, it becomes retrospectively chargeable. In this case, tax will be chargeable on the value of the PET at the date it was actually made, based on the donor’s seven year cumulation (at that date) but using the death rates in force at the date of death, subject to a taper relief.

What is taper relief?

Taper relief reduces the tax on lifetime gifts if the donor survives at least 3 years.

It works on a sliding scale from years three to seven, which means that by the seventh year there is usually no inheritance tax to pay – but the relief only applies to the value of gifts over the Inheritance Tax nil rate band

In the context of a Potentially Exempt Transfer, the taper means that if the donor survives for at least three years, only a reduced percentage of the full death rates will be used as follows:

| Years between gift and death | Percentage of full charge at death rates |

| 0-3 | 100% |

| 3-4 | 80% |

| 4-5 | 60% |

| 5-6 | 40% |

Although the taper relief reduces the amount of tax payable, it does not reduce the value of the transfer for the purposes of the donor’s cumulation. The full value of the transfer is included in the donor’s cumulation for the purposes of working out the death tax on the estate.

The current nil-rate band is £325,000. IHT is charged at a rate of 40% on the chargeable value of an estate (above the nil-rate band) after taking into account the value of any chargeable lifetime transfers.

It’s important to remember that taper relief does not reduce the value of the gift transferred, it only reduces the tax payable.

How does Capital Gains Tax work with gifts?

Capital Gains Tax (CGT) is charged on the ‘gain’ made on non-cash gifts when these assets are sold, such as property (other than your main home), shares and personal possessions worth at least £6,000, with the exception of cars.

When gifting property to children and other assets, they will only need to work out whether they need to pay CGT if they later dispose of the asset.

A transaction can be subject to both Capital Gains Tax and Inheritance Tax, and in this case some double tax relief may be available. In calculating the loss to the estate, no account is taken of any CGT (or any stamp duty or additional expenses) borne by the recipient of the value transferred.

In short, Capital Gains Tax is a tax on the profit received when you sell or dispose of an asset that has increased in value. The gain, or the profit, is taxed, not the amount of money you receive. For example, if you bought a painting for £1,000 but it sold for £30,000 then the gain is £29,000. You will only pay Capital Gains Tax if all your gains in a year exceed the threshold (£6000 in 2023-24).

What does ‘disposing of an asset’ mean?

Disposing of an asset is currently defined as the following for the purposes of Capital Gains Tax:

- Selling the asset

- Giving the asset away as a gift, or transferring it to someone else

- Swapping the asset for something else

- Receiving compensation for the asset, for example the insurance pay out if a property was lost or destroyed

You might wonder what would happen if you sold your asset for a value less than the market value to a family member, to avoid paying CGT. This is not advisable. HMRC will view this as a gift of the asset to a “connected person” – which includes children, parents, siblings, nephews, uncles etc.

To avoid this, the asset needs to be sold at the market value. An asset sold to a connected person at a value less than market value will result in HMRC asking you for CGT as if the property was being paid for at market value. Not only will you have to pay the tax on the full gain, you could also be fined.

IHT exemptions on gifts made out of normal expenditure

After your death, the executors of your estate will need to complete the table on HMRC’s ‘Gifts and other transfers of value’ (IHT 403) form. It is designed to show HMRC your net income versus your net expenditure for the year in which your executors claim you made the regular gift. It will also confirm if there was any surplus income available.

It can be really difficult for the executors to document this information unless you keep a record of it yourself. This is why it’s especially important to keep accurate records of regular gifting so that your loved ones can make use of this IHT exemption. The rules around this exemption are complicated, so we would strongly recommend that you seek financial advice.

Can my grandchild benefit from my Over 50s life insurance policy?

Yes, if you take out your over 50s life insurance policy in trust, your grandchildren can be made beneficiaries and won’t be liable for IHT if a valid claim is made, as the cash sum won’t be counted as part of your estate.

How else can I give my grandchildren tax-free gifts?

Other options could include contributing to a Junior ISA (Independent Savings Account) for your grandchild. While you can’t set this up unless you have parental duties, you can contribute after the account has been opened. These tax-free savings accounts have an annual limit of up to £9,000 (2023-24 tax-year). It is possible to invest in cash or stocks and shares with a Junior ISA, which your grandchild can access on their 18th birthday.

Another option would be to contribute £2,880 to a pension. The child will benefit from 20% tax relief on top of this, taking the total to £3,600 a year into their child's pension, which can take the form of a self-invested personal pension (Sipp), or a stakeholder pension, among other types.

The disadvantage is that the money will be tied up until the child is in their late fifties. While having a nest egg ready for retirement may be a prudent measure, it could prove frustrating having a pension pot that can only be accessed at retirement when in most cases there may be a clear need for the funds earlier in life e.g. to get their foot on the property ladder, start a business, go travelling, buy a car or pay off a student loan.

You should always speak to a professional if you need more information or help in making a decision.

So, how much can you gift your grandchildren? The answer, of course, depends on whether they’ve got wedding bells on the horizon, but in normal circumstances, you can gift many thousands of pounds a year through large and small gifts, pension contributions, and yes, plenty of presents and pocket money.