Types of life insurance

There is more than one type of life insurance, so how do you know which policy is right for you? To the uninitiated, the variety of life insurance policies that are available can make picking the right one a little daunting. In this guide, we’ll explain the main types of life insurance and what kind of customer they might be best suited to.

Where we talk about ‘premiums’ in this article, that means the payment you make for a policy

Life insurance explained

Life Insurance is a financial product that could mean your loved ones receive a sum of money if you were to pass away while covered by the policy. In broad brushstrokes, there are two main types of life insurance: term life insurance and whole of life insurance. Later, we'll look at different types of life insurance within those definitions, but lets start with the big two:

Term life insurance

As a rule of thumb, term life insurance provides financial cover against death for a set period. As the applicant, you choose how much cover you need, and the duration of the policy length, which may cover the length of a mortgage, or other life milestones like your children’s school years. With this type of life insurance, you will only receive your payout if you pass away or have a qualifying terminal illness during the chosen term.

Whole of life insurance

In contrast, whole of life cover provides lifetime coverage, which means your loved ones are guaranteed a payout whenever you die, providing the claim is valid. This is unlike other types of life insurance which cover you for a fixed number of years. The cost of this type of life insurance will reflect the fact the provider will expect to pay out on a valid claim, whenever death may occur. This type of insurance may also be referred to as Life Assurance. The word ‘assurance’ is used because you’re assured that a valid claim will be paid regardless of when you die, so long as you pay your premiums.

Read more about the difference between life insurance and life assurance.

This article mostly focuses on term life insurance. As we will explore, there are different types of life insurance within this category to meet different needs.

Types of term life insurance

Here is more information about the main types of term life insurance:

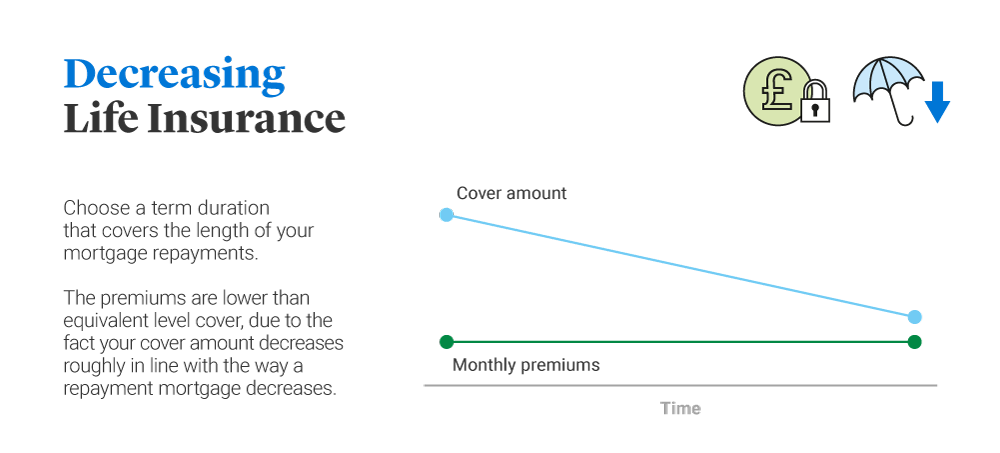

Decreasing life insurance

For many people, the first time they talk about life insurance is when they first take out a mortgage. In this instance, you could choose protection to help cover your repayment mortgage. Before deciding what is right for you, it's worth understanding the difference between life insurance and 'mortgage life insurance'.

Decreasing term life insurance, sometimes known as mortgage life insurance, means your cash sum decreases roughly in with the way a repayment mortgage decreases, though the premiums stay the same unless changes are made to the policy. The upshot is that you can choose the exact amount of cover for your needs, and the premiums are lower compared to level cover, due to the fact the cash sum reduces over time.

Pros and cons of Decreasing Life Insurance

| Pros | Cons |

|---|---|

| Will generally cost less than an equivalent level term policy | If you need to cover more than a repayment mortgage, remember that the payout will decrease over time |

| Flexibility – you choose how much cover you need and how long for | You will need to check that the interest rate on your mortgage does not become higher than the rate applied to the policy. |

| Add-ons available like Critical Illness Cover for an extra cost | If used to cover your mortgage, your policy may not completely pay off your outstanding mortgage unless you make sure your amount of cover is adjusted to match any new mortgage arrangements |

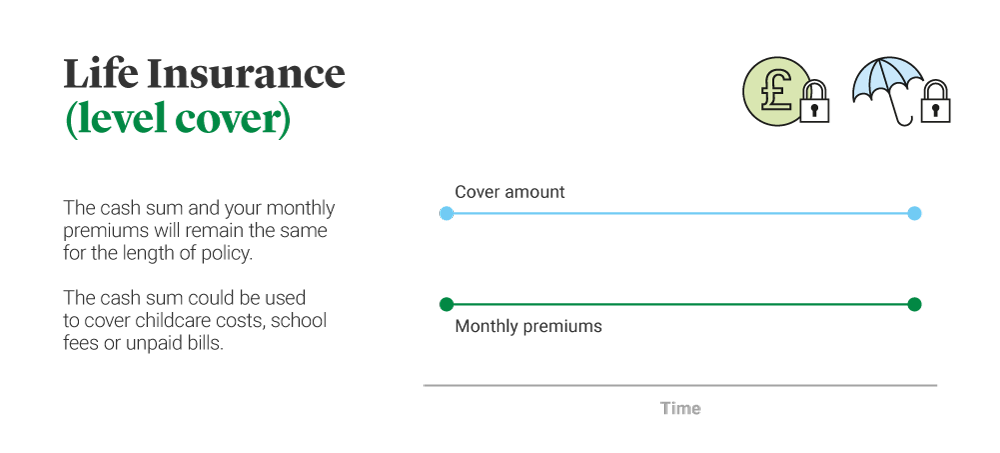

Level term life insurance

For many households, a ‘level’ policy is the best type of life insurance as the cash sum stays the same throughout your policy term, and your monthly premiums will remain the same unless you make a change to your policy.

Read more about the difference between mortgage insurance and life insurance.

What does a level term life insurance policy cover? The cash sum could be used for any purpose, for example to cover the mortgage, childcare costs, school fees or unpaid bills. If your children, partner or other relatives depend on you financially and your parental responsibilities, this type of policy could help financially protect your family if you passed away.

Pros and cons of level term life insurance

| Pros | Cons |

|---|---|

| Your potential payout remains the same during the policy term | Can cost more than an equivalent decreasing life insurance |

| Protect a range of expenses, including the mortgage/rent, bills and childcare costs | Any payout doesn’t increase with inflation |

| Add-ons available like Critical Illness Cover for an extra cost | The payout could be subject to Inheritance Tax. You can avoid this by placing your policy in Trust.

|

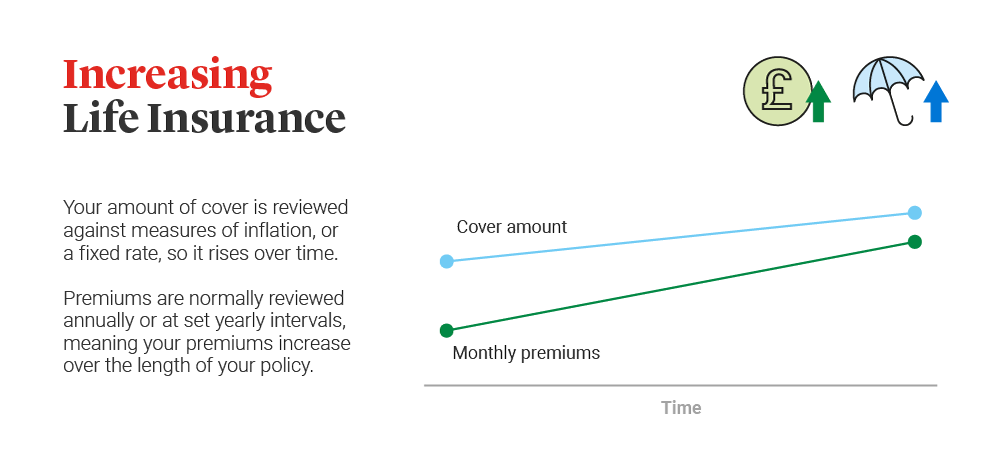

Increasing term life insurance

Perhaps one of the lesser known types of life insurance policy is ‘increasing term life insurance’. This means you pay higher premiums over the length of your cover but your cover amount is reviewed against measures of inflation, or a fixed rate so it rises over time. Premiums are normally reviewed annually or at set yearly intervals. This type of life insurance is normally designed to protect against inflation and the rising costs of living. This type of policy is only sold via our team of advisers. You can call them on 0800 197 9208. Call charges may apply.

Pros and cons of increasing life insurance

| Pros | Cons |

|---|---|

| Your potential payout keeps pace with the rising cost of living | Your premiums rise during the policy term as inflation increases |

| As with level term policies, any payout could cover a wide range of living expenses | Likely to be more expensive than a standard ‘level term’ or decreasing life insurance policy |

| Peace of mind regardless of rising living costs. | Premiums are usually reviewed annually (not monthly or quarterly) |

Critical Illness Cover

Anyone can experience a critical illness at any time. And if this happens to you while protected by critical illness cover, a successful payout could lessen the financial impact on your family. But how does this type of cover work?

Legal & General’s Critical Illness Cover can be added for an additional cost when you take out Life Insurance or Decreasing Life Insurance. It could pay out a cash sum if you're diagnosed with, or undergo a medical procedure for one of the specified critical illnesses that we cover during the length of your policy, and you survive for 14 days from diagnosis.

Refer to our guide about how the cover works and how much you might need.

Pros and cons of critical illness cover

| Pros | Cons |

|---|---|

| It could provide financial support to help you adjust after a potentially life changing illness or operation | Cover is available for specified illnesses only and you must meet our definition of the illness |

|

Covers a broad range of critical illnesses, including heart attack, stroke and many types of cancer |

Only available for extra cost |

|

Children's Critical Illness Cover is automatically included. Terms and conditions apply. |

Conditions apply, such as the minimum number of days an insured person must live following a diagnosis before a payout can be made. |

Terminal Illness Cover

A terminal illness is a difficult scenario for anyone to imagine, but financial protection is available in the form of terminal illness cover. Our Terminal Illness Cover is automatically included on Life Insurance with a minimum term of 2 years and Decreasing Life Insurance (which has a minimum term of 5 years). Terminal Illness Cover could pay out the full amount of cover when life expectancy is less than 12 months and you meet our definition of a terminal illness.

Single vs joint life insurance

Additionally, if you take out Life Insurance or Decreasing Life Insurance with or without Critical Illness Cover, you can choose to set this up as either single life insurance or joint life insurance. Here is how these types of life insurance compare:

| Single life insurance | Joint life insurance |

|---|---|

| Covers one person only | Covers two lives |

| Couples can have two single policies | Pays out on a ‘first death’ basis |

| Often more expensive, but both policies would pay out in the event of a valid claim | Often cheaper, but only pays out once |

A single policy covers one person and pays out following a valid claim during the length of the policy, at which point the cover ends. Some couples decide to take out two single policies so that the surviving partner still has cover after the death of the first person.

By contrast, joint life insurance covers two lives, but will only pay out once the first person dies or is diagnosed with a terminal illness (or specified critical illness if critical illness cover is chosen) and meets our definition during the length of the policy. It may be cheaper to get joint life insurance, but for some households, both partners may need cover.

Over 50s Life Insurance

So far we’ve covered types of term life insurance, but the one exception on our list is over 50s life insurance – a type of ‘whole of life’ cover. Our Over 50s Fixed Life Insurance is for people aged 50 to 80, and comes with guaranteed acceptance and no medical questions. 100% of claims are paid, and the money can be put towards funeral costs or a small gift to loved ones when the policyholder passes away. You can compare Over 50s Life Insurance policies with this guide.

Pros and cons of Over 50s Life Insurance

| Pros | Cons |

|---|---|

| Guaranteed acceptance and full cover after one year – with no medical | The premiums you pay might exceed the cash sum itself |

| Premiums are fixed and the cover will never go down | The policy has no cash value unless a valid claim is made |

| Most claims are paid in one day | The cash sum is fixed and won’t rise with inflation. |

Who can benefit from different types of life insurance?

Every life insurance applicant has different needs, but to give you a sense of which policy or option could help with your protection needs, we've put together the table below.

| Types of life insurance | Who could it benefit? |

|---|---|

| Level term life insurance | Designed for people who need a policy that provides a cash sum to help financially support their family in the event of death, terminal illness or critical illness (if chosen). |

| Decreasing life insurance | Designed for people who have a repayment mortgage and need a policy that pays out a cash sum, which decreases roughly in line with the way a repayment mortgage decreases, helping to protect their mortgage in the event of death, terminal illness (if life expectancy is less than 12 months), or critical illness (if chosen). |

| Critical illness cover | Designed to pay out a cash sum sum if the person covered is diagnosed with a specified critical illness that we cover, during the policy. |

| Whole of life insurance | Designed for people who need a policy that provides a lump sum on their death. Helping to give financial support to their family, which could be used to help towards an expected Inheritance Tax bill – impacting their lifestyle and everyday living expenses. |

| Increasing life insurance | Designed to protect against inflation. Every year, we’ll give the person covered the option to increase the amount they are insured for, in line with any changes in the Retail Prices Index (RPI) without the need for further medical evidence. If this option is chosen, the premium will also increase |

| Over 50s life insurance | Designed for those who want guaranteed acceptance with no medical, who are aged 50-80 and want to leave a lump sum to loved ones after their death. |

Other types of term life insurance

In addition, you may hear the term renewable term insurance, which means you can extend your term without having to undergo a new medical examination, or new underwriting. With this type of life insurance, you may have to pay higher premiums as you get older, and there will be a renewal limit. If your term life insurance can be converted into a whole-of-life arrangement, then you have a convertible life insurance policy. Legal & General do not offer these types of cover.

What life insurance should I get?

We hope we've explained life insurance in a simple as way as possible. Ultimately, the best type of life insurance is the policy that matches you and your loved one’s needs, providing the right amount of cover at a price you can afford.

If you have particular requirements about the kind of life insurance you need, you can contact Legal & General and speak to a financial adviser.

Find out more about the types of life insurance we offer:

Its important to remember that life insurance is not a savings or investment product and has no cash value unless a valid claim is made.